APAC Wrap: 17 April 2026

Hello,

In my second week working with FundaAI, we have published a note on TPUs, now Funda’s most read work on Substack.

I have noticed the views there echoed in a few other places, like this academic paper:

"The dominant constraints on AI systems are shifting from raw compute capability to data movement, connectivity, energy efficiency, system-level integration, and cost effectiveness (e.g., $/token)."

"Connectivity is as critical as computation: Performance scaling increasingly depends on interconnect bandwidth, latency, and topology, requiring connectivity–compute co-design rather than treating networking as a secondary concern."

Fabian also made a similar comment on this back in December:

For years the semiconductor industry measured progress in FLOPs. More compute, faster chips, bigger clusters. That framing is now incomplete. The real constraint in modern AI infrastructure is not how fast individual GPUs compute. It is how fast thousands of them can share data with each other.

Kioxia: YMTC has three factories on the way that will more than double production (RT)

Funda also published a piece on Kioxia last week.

Kioxia has reportedly started operations at the second Kitakami building (K2) in September 2025, installing equipment and expanding cleanroom areas to further boost production.

We’ll be looking out for what they have to say about capital returns on their investor briefing in June.

Sentiment has recently been weighed down by reports of YMTC’s expansion plans:

Expansion: Each of the three new plants will produce 100,000 wafers per month.

Current Capacity: YMTC currently produces a combined 200,000 wafers per month from its first two fabs.

Self-Sufficiency: Over 50% of the equipment for the third factory (Wuhan) is sourced from domestic Chinese companies. The third factory has been completed and is currently installing equipment.

DRAM Entry: YMTC is also pivoting into DRAM; all three new plants will allocate some capacity to memory chips. The exact amount will depend on the company’s progress in developing those chips.

Another Chinese article continued to weigh on the stock today:

“Yangtze Memory Technologies Co., Ltd.’s revenue in the first quarter of this year exceeded 20 billion yuan, more than doubling year-on-year. Its NAND (flash memory) chip production has exceeded 10% of the global market share, approaching the third largest in the world,” said a core person in the memory chip industry chain. “The profits will be even more explosive in the future.”

Chinese imports of US chip tools from Singapore and Malaysia hit record (Nikkei Asia)

According to Nikkei Asia, Chinese imports of US chip tools from Singapore and Malaysia in 2025 have hit record highs.

Singapore: $5.7 billion (up 17% YoY).

Malaysia: $3.4 billion (more than double the 2024 figure).

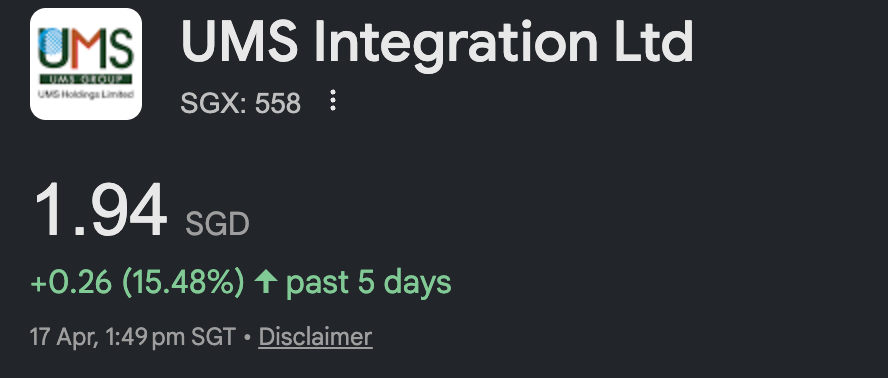

Lam Research is significantly expanding its manufacturing footprint in Malaysia. We believe UMS Integration’s facility (serving Lam) is currently at 50% utilization. The stock gained roughly 15% this week.

Some good news for Lam and Tokyo Electron too in the revised MATCH bill reported by Reuters here.

Hansol Group makes a small acquisition to enter the DRAM probe card market

Hansol is acquiring an 83.37% stake in Will Technology for ₩177.2 billion KRW (~US$120.6 million), implying a total valuation of US$144.6 million.

Will Technology is the #1 provider of probe cards for Samsung’s Galaxy S series APs and CIS (image sensor chips).

Hansol plans to use this acquisition to enter the DRAM probe card market and expand into China.

Valuation: We estimate this implies a P/E of ~24.4x and a P/S of ~3.15x. This might be seen as a rich valuation for a new entrant compared to established Japanese peers like JEM (6855).

Special thanks to one of our readers for flagging this.

Macronix thesis playing out elsewhere in Taiwan

In brief, the Macronix (2337.TW) thesis is that it is emerging as a highly profitable monopoly in the eMMC memory market as the "Big Four" memory giants abandon this market and reallocate their capacity toward high-margin HBM and high-end NAND flash.

There appears to be a similar play in another industry: