APAC Wrap: 5 June 2026

Hello from Taipei.

It has been a very productive week at Computex - Fabian and I met Semi-Twitter celebrities and supply chain sleuths, and refined our booth-hopping technique.

It will take some time to piece together and digest all our notes. In the meantime:

The FundaAI team is tracking implications for the likes of Marvell, Intel, AMD, Qualcomm, Micron, Sandisk and Kioxia. Also in the background we have analysts dropping notes on Coherent Lite, NPO (institutional report), and Cybersecurity.

Funda also tracks revenue growth at frontier AI labs, now getting more attention because Sam said token costs is becoming a “huge issue”.

We have at least one new pick for this newsletter arising out of Computex, could well be our pick for June. It has barely run up despite being in a very hot space right now.

Memory: SA plot twist; Jensen in Korea; Only YMTC and Kioxia adding Nand capacity

So the SA note yesterday carried the rather bearish headline:

Thanks for the Memories - VR NVL72 SOCAMM DRAM Capacity per rack Cut in Half.

But ends with:

We believe the reduction in SOCAMM content for Vera Rubin is being driven by constrained DRAM supply across all three memory suppliers.

Also not sure what the market is doing selling off Hynix and Samsung when Jensen is Korea and when the media feels like it needs to report what he is eating:

Samgyeopsal (pork belly) and soju are the likely dinner menu items.

Separately, Jukan reported today that SK Hynix is not adding Nand capacity:

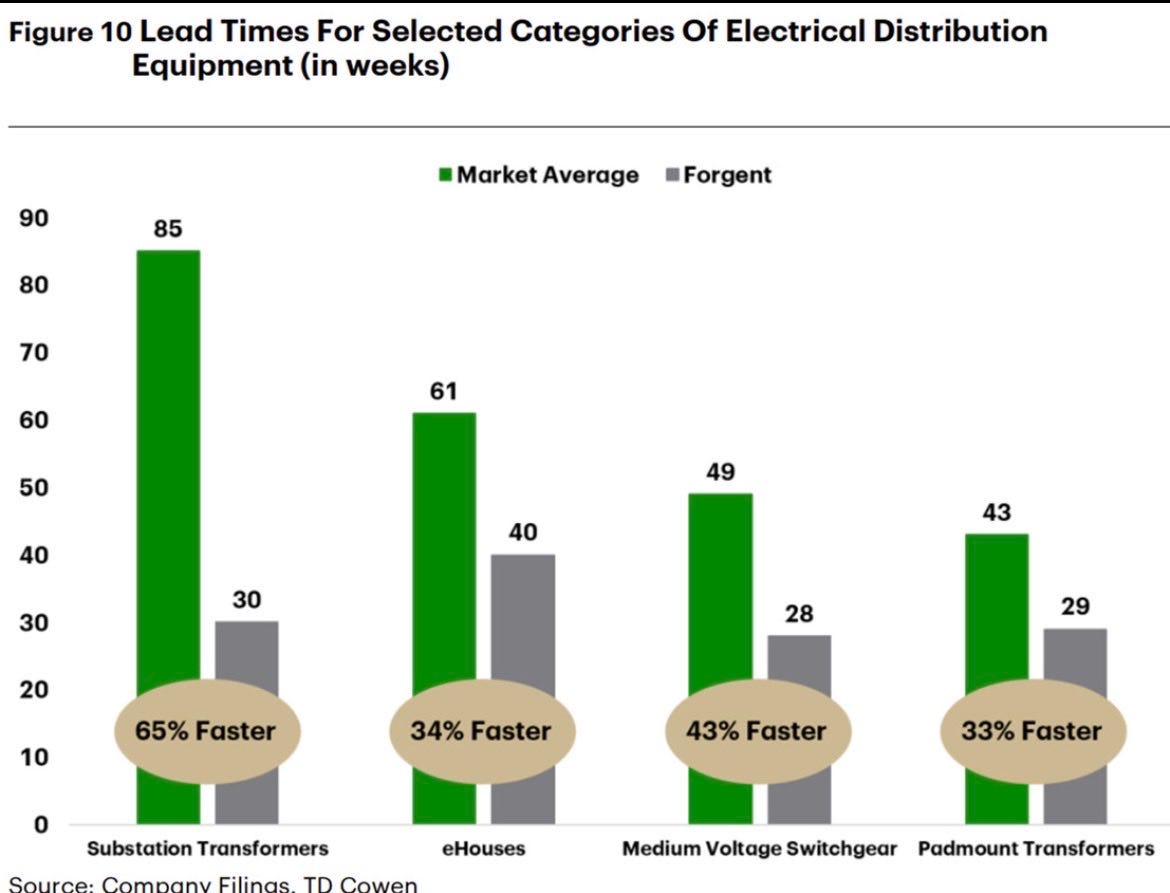

FPS: +8% yesterday

We hit the double on FPS yesterday since we first flagged it in the chat. Thanks again to Guasty Winds for the tweet about it dropping below $30.

We have also been helped by the White House designating electrical infrastructure as essential to national defence as well as this chart:

We are going to comp folks for great contributions like this going forward.

Victory Giant: -11% as US weighs subsidies to boost domestic PCB manufacturing

Some attributing to this story.

From the chat: